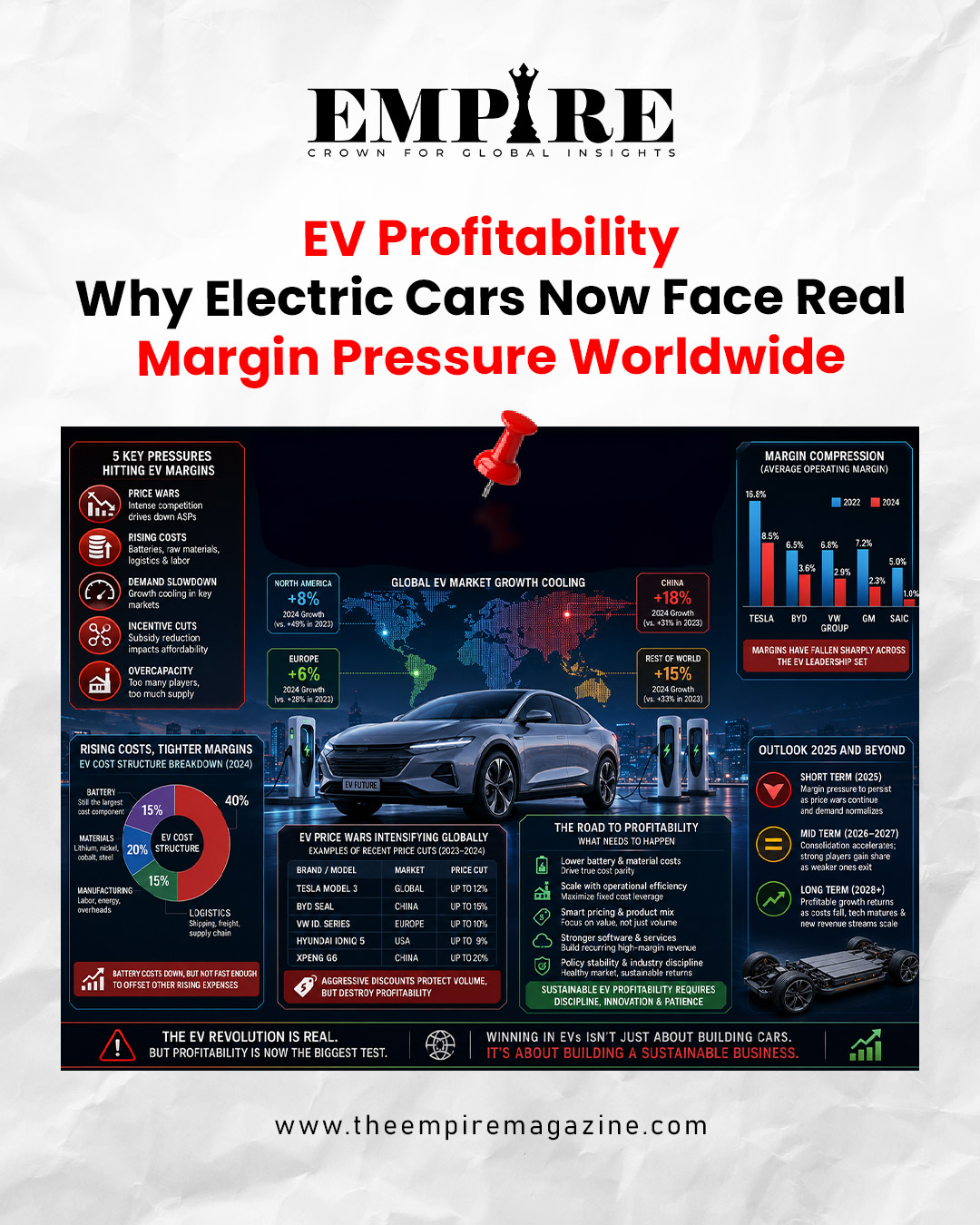

Electric vehicles have spent the past decade rewriting the rules of the automotive industry. Governments introduced ambitious clean mobility policies, investors poured billions into battery technology, and consumers embraced the idea of driving without tailpipe emissions. For a while, the narrative seemed almost unstoppable. Every quarter brought announcements of new EV launches, record-breaking valuations, and aggressive production targets. Yet as the global market matures, the conversation has shifted from growth to profitability. Selling electric cars is no longer simply about producing more vehicles, it is about earning sustainable margins in one of the world’s most competitive industries. Automakers that once celebrated rapid expansion are now confronting shrinking profits, rising production costs, fierce price wars, and increasingly cautious consumers. The challenge is not a lack of demand alone. Instead, manufacturers are discovering that scaling an electric vehicle business while protecting profitability is significantly harder than initially expected. As competition intensifies across North America, Europe, China, and emerging markets, the global EV industry is entering a new phase where financial discipline matters as much as technological innovation. The companies that survive this transition will not necessarily be those that sell the most vehicles but those capable of balancing affordability, innovation, operational efficiency, and long-term shareholder value. The race has moved beyond electrification itself and toward building a profitable business model that can withstand economic uncertainty and changing market dynamics.

Price Wars Are Squeezing Every Automaker

One of the biggest reasons behind mounting margin pressure is the global price war unfolding across the electric vehicle market. Major manufacturers have repeatedly reduced prices to maintain sales momentum, forcing competitors to respond with discounts of their own. While lower prices have helped attract buyers, they have also significantly reduced per-vehicle profits. Unlike traditional internal combustion vehicles, EVs still rely heavily on expensive battery systems, sophisticated software, advanced semiconductors, and specialized manufacturing processes. When selling prices decline faster than production costs, profit margins inevitably narrow. Chinese manufacturers have intensified this challenge by offering technologically advanced vehicles at highly competitive prices, increasing pressure on established global brands. At the same time, legacy automakers continue investing billions in dedicated EV platforms, battery factories, charging ecosystems, and software development while simultaneously supporting conventional vehicle operations. This dual investment cycle places enormous strain on financial performance. Investors who once rewarded aggressive EV expansion are increasingly demanding positive cash flow, higher operating margins, and measurable returns on capital. As a result, executives are finding themselves under pressure to deliver profitable growth rather than growth at any cost. The market is becoming less forgiving, and every pricing decision now carries significant financial consequences. Companies must carefully balance affordability for consumers with the need to recover massive research, development, and manufacturing investments that often take years to generate meaningful returns.

Rising Costs Continue to Challenge EV Economics

While battery prices have gradually declined over the past decade, producing electric vehicles remains an expensive undertaking. Lithium, nickel, cobalt, copper, and rare earth materials continue to experience periodic price volatility due to geopolitical tensions, mining constraints, and growing global demand. Although manufacturers are investing heavily in battery recycling and alternative chemistries such as lithium iron phosphate, supply chain uncertainties continue to influence production costs. Beyond batteries, software development has emerged as another major expense. Modern electric vehicles increasingly function as connected digital platforms requiring continuous software updates, cybersecurity protection, artificial intelligence features, autonomous driving capabilities, and cloud-based services. Maintaining these digital ecosystems demands substantial long-term investment that extends well beyond the initial vehicle sale. Manufacturing facilities also require significant modernization, including highly automated assembly lines, dedicated battery integration systems, and new quality control processes. Meanwhile, higher interest rates in several economies have increased financing costs for both manufacturers and consumers, making EV purchases less affordable despite government incentives. Consumer expectations have also evolved rapidly. Buyers now expect longer driving ranges, faster charging, premium infotainment systems, and advanced driver assistance technologies without accepting substantially higher prices. Meeting these expectations while protecting profitability has become one of the industry’s greatest strategic challenges. Manufacturers must constantly improve efficiency, negotiate better supplier agreements, and streamline production without compromising safety, quality, or innovation.

Global Competition Is Redefining the Industry

The competitive landscape has transformed dramatically as new manufacturers enter international markets with aggressive expansion strategies. Chinese electric vehicle companies have rapidly improved product quality while maintaining cost advantages through vertically integrated supply chains and large-scale battery production. Their growing presence is encouraging traditional manufacturers to accelerate innovation while simultaneously defending market share through pricing incentives and new product launches. Meanwhile, established automotive companies face the difficult task of transitioning decades-old manufacturing ecosystems toward electrification without disrupting existing revenue streams generated by gasoline and diesel vehicles. This balancing act requires careful capital allocation, workforce reskilling, dealer network transformation, and continuous technological upgrades. Regional differences further complicate profitability. Europe faces tightening emissions regulations alongside slowing consumer demand in certain segments, while North America continues expanding charging infrastructure but remains sensitive to interest rates and vehicle affordability. Emerging markets present enormous long-term opportunities, yet infrastructure limitations and price sensitivity make rapid adoption challenging. Governments are also gradually shifting from generous purchase subsidies toward broader industrial policies focused on domestic manufacturing and supply chain resilience. As incentives evolve, automakers must increasingly rely on competitive products rather than policy support to drive sales. Success will depend on operational excellence, localized production, battery innovation, software differentiation, and strategic partnerships that reduce costs while improving customer value. The companies capable of adapting quickly to regional market realities will be better positioned to protect profitability even as competition continues to intensify.

The Future Belongs to Sustainable Profits, Not Just Sales

Electric vehicles remain central to the future of global mobility, but the industry’s next chapter will be defined less by headline-grabbing sales numbers and more by sustainable financial performance. Investors, policymakers, suppliers, and consumers increasingly recognize that long-term success requires healthy business fundamentals alongside environmental progress. Automakers are therefore focusing on improving manufacturing efficiency, simplifying vehicle architectures, expanding battery recycling, localizing supply chains, and generating recurring revenue through connected services and software subscriptions. Artificial intelligence is also helping manufacturers optimize production planning, predictive maintenance, inventory management, and quality assurance, creating opportunities to reduce operational costs without sacrificing customer experience. At the same time, innovation in solid-state batteries, next-generation power electronics, and modular vehicle platforms promises to improve efficiency while lowering production expenses over the coming decade. Consumer confidence will remain equally important. Reliable charging infrastructure, competitive financing, transparent ownership costs, and dependable after-sales support will influence purchasing decisions as much as technological specifications. Ultimately, the electric vehicle revolution has entered a more mature and demanding phase. Winning the market will no longer depend solely on producing attractive electric cars but on building resilient businesses capable of delivering innovation, affordability, and consistent profitability simultaneously. As global competition reshapes the automotive landscape, manufacturers that combine disciplined financial management with continuous technological advancement will define the future of sustainable transportation. For the EV industry, the road ahead remains promising, but profitability, not production alone, will determine which companies lead the next generation of mobility.

For more business and retail insights, read more on The Empire Magazine

Previous article: Cloud Giants

Magazine Feautures | Podcasts: Empire Global Talks

Follow The Empire Magazine on Facebook | Instagram | LinkedIn

The Empire Magazine | Crown for Global Insights