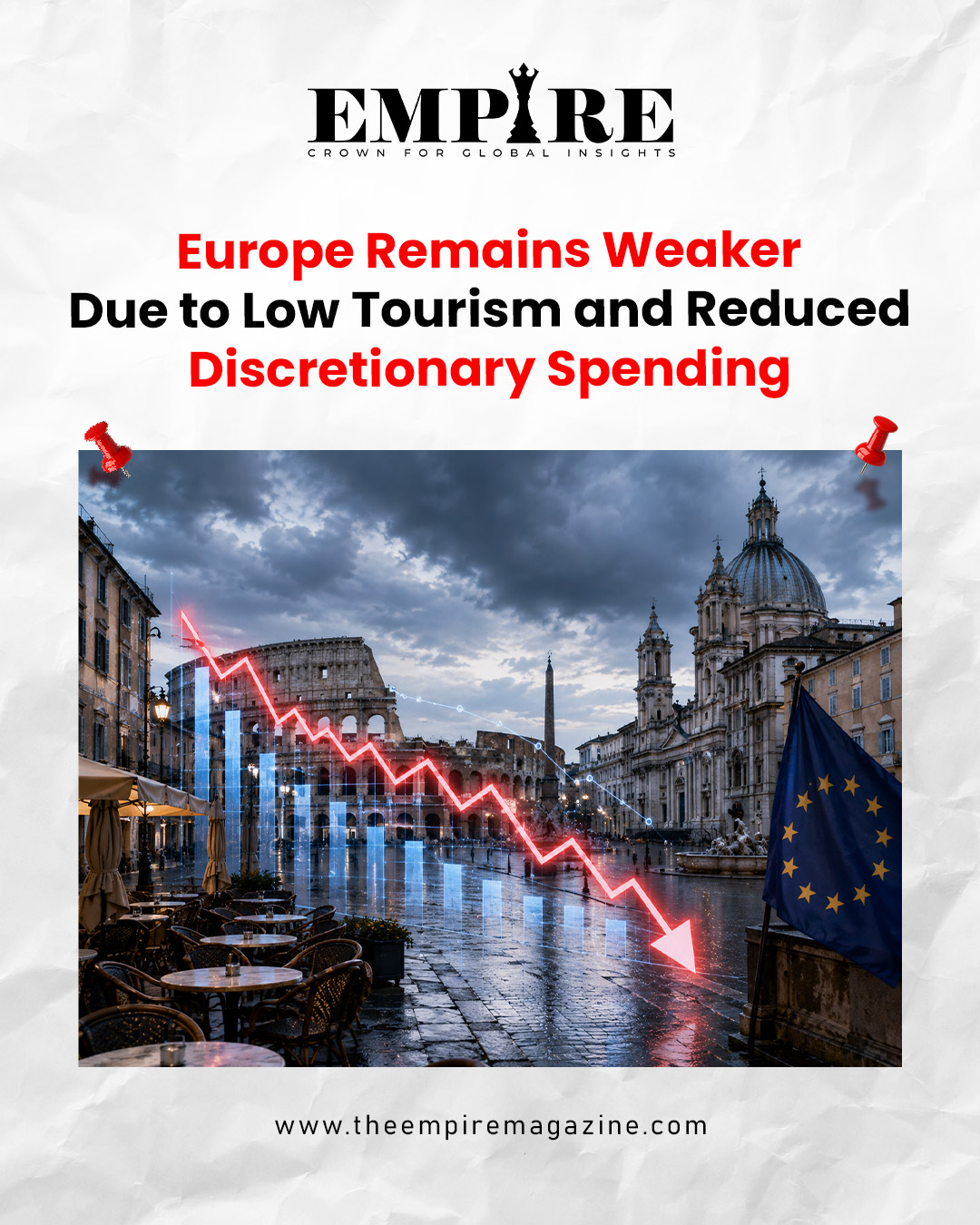

Europe remains weak as low tourism and reduced discretionary spending continue to weigh on the region’s economic recovery. After years of navigating inflation, geopolitical uncertainty, high borrowing costs, and changing consumer priorities, Europe’s hospitality, retail, luxury, aviation, and entertainment sectors are experiencing slower-than-expected demand. While several economies have managed to avoid recession, consumer confidence remains fragile, leaving businesses cautious about expansion and investment. Across major destinations, fewer international visitors, lower household spending, and restrained purchasing behaviour are creating ripple effects that extend far beyond tourism. As governments, retailers, airlines, and investors closely monitor evolving economic indicators, the challenge is no longer simply attracting visitors, it is rebuilding consumer confidence. The coming months will determine whether Europe can regain momentum or whether the continent will continue facing slower growth compared to other global regions.

Europe Remains Weak Amid Consumer Caution

Europe remains weaker because consumers are increasingly prioritising essential expenses over discretionary purchases. Although inflation has moderated compared to its peak levels, prices across housing, utilities, transportation, groceries, and services remain significantly higher than they were before the pandemic. Many households continue adjusting their monthly budgets to cope with elevated living costs, leaving less disposable income for travel, shopping, dining, entertainment, and luxury purchases. Interest rates, while expected to ease gradually, have also increased mortgage and loan repayments for millions of families, reducing their financial flexibility. This cautious behaviour is reflected in slower retail sales, weaker hospitality revenues, and lower demand across several consumer-driven industries. Businesses that once relied on spontaneous consumer spending are now witnessing customers researching purchases more carefully, delaying vacations, shortening travel itineraries, and choosing value-focused alternatives instead of premium experiences. These behavioural shifts are changing the broader economic landscape, making consumer confidence one of the most closely watched indicators across Europe. Until households regain confidence in their financial future, discretionary spending is likely to remain under pressure, slowing the pace of overall economic recovery.

Europe Remains Weak as Tourism Slows

Europe remains weaker as international tourism continues to recover unevenly despite the reopening of global travel markets. Southern destinations such as Spain, Italy, Portugal, and Greece continue attracting significant visitor numbers during peak seasons, yet many urban business destinations and several Central European markets are witnessing slower recovery compared to pre-pandemic levels. Business travel has not fully returned as companies increasingly rely on virtual meetings and tighter travel budgets. Additionally, long-haul travellers from Asia have returned more gradually than expected, while many North American visitors are shortening their European vacations due to higher travel costs and currency fluctuations. Airlines, hotels, restaurants, museums, local transport providers, and independent retailers all depend heavily on tourism-generated spending, making reduced visitor activity a broader economic challenge rather than an isolated industry issue. Seasonal tourism alone cannot compensate for weaker year-round visitor flows, leaving many businesses operating below optimal capacity. Tourism remains one of Europe’s largest employment generators, meaning slower visitor growth also affects hiring, wages, local investment, and regional development across numerous economies.

Europe Remains Weak Due to Reduced Discretionary Spending

Europe remains weaker because discretionary spending has become one of the biggest casualties of prolonged economic uncertainty. Consumers are increasingly postponing purchases that are considered optional, including luxury goods, fashion, electronics, home improvements, premium dining, and leisure activities. Rather than making impulse purchases, households are comparing prices, seeking discounts, and waiting for promotional periods before committing to major expenditures. Retailers across Europe have responded by increasing discounts earlier than usual, adjusting inventory strategies, and introducing more affordable product lines to stimulate demand. However, discounting also compresses profit margins, limiting investment capacity for many businesses. Reduced discretionary spending particularly affects sectors that depend on aspirational purchases, where emotional buying behaviour typically drives revenue growth. Even affluent consumers have become more selective, reflecting broader concerns about future economic conditions. While employment remains relatively resilient across several European economies, wage growth has not always kept pace with cumulative inflation, leaving consumers more cautious about spending. This shift represents a structural change rather than a temporary slowdown, requiring businesses to rethink pricing, marketing, and customer engagement strategies.

Europe Remains Weak Across Retail and Luxury

Europe remains weaker across retail and luxury markets as premium brands experience softer consumer demand compared to previous years. Luxury shopping has historically benefited from international tourists, particularly visitors from China, the United States, and the Middle East. Although travel has resumed, shopping patterns have changed significantly. Consumers are purchasing fewer high-value items, focusing more on experiences than material goods, and spreading spending across multiple destinations instead of concentrating purchases in traditional luxury capitals. Department stores, designer boutiques, and premium fashion brands are adapting by strengthening digital commerce, investing in personalised customer experiences, and expanding loyalty programmes to retain high-value customers. Retailers are also increasingly relying on artificial intelligence for inventory forecasting, personalised recommendations, and demand prediction to improve operational efficiency. Meanwhile, mid-market retailers face pressure from both discount chains and premium brands, creating intense competition across nearly every consumer category. Shopping habits continue evolving as consumers seek greater value, sustainability, and product longevity, forcing businesses to innovate beyond pricing alone.

Europe Remains Weak Despite Stable Employment

Europe remains weaker despite relatively stable employment figures because economic confidence depends on more than job availability. Many consumers remain concerned about future income stability, taxation, energy costs, and geopolitical developments. Ongoing international conflicts, supply chain adjustments, energy market volatility, and political uncertainty continue influencing household financial decisions. Businesses are similarly cautious, delaying expansion plans, reducing recruitment, and limiting capital expenditure until stronger consumer demand becomes visible. Small and medium-sized enterprises are particularly vulnerable because they often lack the financial reserves available to multinational corporations. Banks have also tightened lending standards, making business financing more challenging for entrepreneurs and growing companies. Consumer psychology plays an increasingly important role in shaping economic performance, as confidence directly influences purchasing behaviour, investment decisions, and business activity. Even when macroeconomic indicators appear relatively stable, cautious consumer sentiment can significantly slow overall economic momentum, reinforcing the perception that Europe remains weaker compared to faster-growing global regions.

Europe Remains Weak as Businesses Adapt

Europe remains weaker, but businesses are responding through innovation, operational efficiency, and digital transformation. Companies across hospitality, retail, aviation, and entertainment are increasingly leveraging artificial intelligence, automation, predictive analytics, and customer data to optimise costs while enhancing customer experiences. Hotels are introducing flexible pricing models, airlines are expanding premium economy offerings, retailers are strengthening omnichannel shopping experiences, and tourism boards are promoting year-round travel instead of seasonal campaigns. Sustainability also continues influencing consumer decisions, encouraging businesses to invest in greener operations and environmentally responsible tourism experiences. Many companies are focusing on domestic travellers alongside international visitors, recognising that diversified customer bases can reduce exposure to external economic shocks. Digital marketing, personalised promotions, subscription services, and loyalty programmes have become central components of long-term business strategies. Rather than waiting for consumer behaviour to return to previous patterns, organisations are redesigning business models to align with changing expectations and evolving market realities.

Europe Remains Weak but Recovery Opportunities Exist

Europe remains weaker today, but several long-term opportunities could strengthen the region’s economic outlook. Falling inflation, potential interest rate reductions, improving wage growth, and continued investment in digital infrastructure could gradually restore consumer confidence. International tourism is also expected to strengthen further as airline capacity expands and travel demand from Asian markets continues recovering. Governments are investing in sustainable transport, digital economies, renewable energy, and infrastructure projects that may stimulate employment and support domestic demand over the coming years. Businesses embracing artificial intelligence, personalised customer engagement, operational resilience, and flexible pricing models are likely to outperform competitors during this transition period. Consumer spending typically improves when households perceive greater financial stability, making confidence restoration a critical objective for policymakers. If inflation continues easing while real incomes improve, discretionary spending could gradually return, supporting retail, hospitality, travel, and entertainment sectors throughout Europe.

The Future of Europe Remains Weak Until Confidence Returns

Europe remains weaker primarily because economic recovery depends as much on confidence as it does on financial indicators. Tourism recovery, consumer spending, business investment, and retail growth are deeply interconnected, meaning weakness in one area often affects the broader economy. While Europe possesses world-class infrastructure, globally recognised brands, strong institutions, and resilient businesses, rebuilding household confidence will remain essential for sustainable growth. Companies that understand changing consumer priorities, invest in innovation, embrace digital transformation, and deliver greater value are likely to emerge stronger as market conditions improve. The continent’s long-term fundamentals remain attractive, but short-term caution continues shaping consumer behaviour and business strategy. As inflation moderates, travel demand gradually strengthens, and economic uncertainty eases, Europe may begin reversing current trends. Until then, the reality remains clear: Europe remains weaker due to low tourism and reduced discretionary spending, making consumer confidence the defining factor in the region’s next phase of economic recovery.

Interconnected factors continue influencing consumer behaviour and business performance

Europe remains weaker not because of a single economic challenge but because several interconnected factors continue influencing consumer behaviour and business performance simultaneously. Lower tourism, cautious household spending, persistent inflationary effects, and evolving purchasing priorities are collectively reshaping Europe’s economic landscape. While the region retains strong long-term fundamentals, sustainable recovery will depend on restoring consumer confidence, encouraging discretionary spending, and supporting tourism-led industries. Businesses that embrace innovation, digital transformation, customer-centric strategies, and operational resilience will be better positioned to navigate this period of uncertainty. As global economic conditions gradually improve, Europe has the potential to regain momentum, but confidence not just economic growth will ultimately determine how quickly the continent returns to stronger and more balanced expansion.

For more business and retail insights, read more on The Empire Magazine

Previous article: https://theempiremagazine.com/ai-regulation/

Magazine Feautures | Podcasts: Empire Global Talks

Follow The Empire Magazine on Facebook | Instagram | LinkedIn | YouTube

The Empire Magazine | Crown for Global Insights